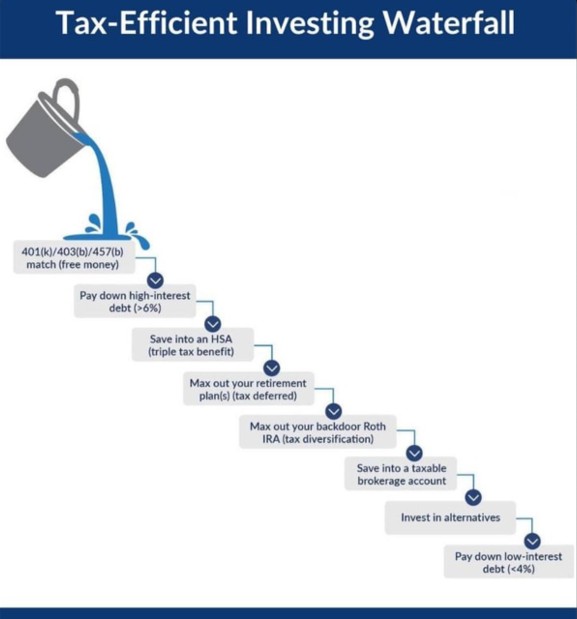

If you’re in a position where your income exceeds your expenses, you have probably asked yourself some form of the following question: what do I do with this excess cash? So many investment options are available it can be overwhelming, so we put together our general guidelines to help. While every person’s situation is different and this protocol may not be one-size-fits-all, we believe it will be helpful to most.

Step 1: Build a small emergency fund

This might be only a few thousand dollars or up to one month of expenses. You just want enough that you can take care of a major expense (car repair, house repair, etc.) without too much worry. You can keep this in your checking account or open a high-yield savings account.

Step 2: Contribute up to your employer’s match in your workplace retirement plan

This is as close to free money as you are going to find. If your employer matches your contributions 1 to 1 up to a certain amount, it is the equivalent of an immediate 100% return on your investment. Assuming an annual return of 10%, it would take the stock market seven years to do that. If you don’t have an employer sponsored retirement plan or your employer does not offer a matching contribution, skip this step.

Step 3: Pay off high-interest debt

Generally, this refers to credit card debt, but could include personal loans, car loans, student loans, etc. Any interest rate over about 8% should likely be paid off as quickly as possible. Start paying off the loan with the highest interest rate first to minimize the interest you pay.

Step 4: Increase your emergency fund

The general rule is to have 3-6 months of expenses available. You will want to keep this in a high-yield savings account or you can use a money market fund in a taxable brokerage account.

Step 5: Contribute to an IRA

If your income is low enough, we recommend contributing to a Roth IRA. If your income is above the point where you can deduct traditional IRA contributions, skip this step (unless you are eligible for a backdoor Roth IRA or mega backdoor Roth IRA – we can help you determine this). If you are eligible for an HSA account, contribute to this plan in this step.

Step 6: Max out your workplace retirement plan

Contribute the IRS maximum allowed for your workplace retirement plan. If you are self-employed, look at opening a SEP IRA, SIMPLE IRA, or Individual 401k. If applicable, consider a 529 plan at this step.

Step 7: Contribute to a taxable brokerage account

Congratulations, you have exhausted all your options to contribute to tax-advantaged accounts (at least without some more complicated maneuvers). You should now open a taxable brokerage account to save for other goals.

What do I invest in?:

Make sure to invest your money in your workplace plan, IRAs, HSAs, and taxable brokerage accounts. When you make the contribution to these accounts, it will stay in cash until you purchase some assets. If you are uncertain which assets to purchase given the overwhelming options available to investors, feel free to ask us for assistance. We can help clients in determining how much risk to take on in their accounts given their unique circumstances and are experts in building portfolios to help our clients meet their goals.

If you have any questions about this blog, or other questions about your finances, please contact Blue River Capital Management at 503.334.0963 or at info@brcm.co.

This information is intended to be educational and is not tailored to the investment needs of any specific investor. Investing involves risk, including risk of loss. Blue River Capital Management does not offer tax or legal advice. Results are not guaranteed. Always consult with a qualified tax professional about your situation.