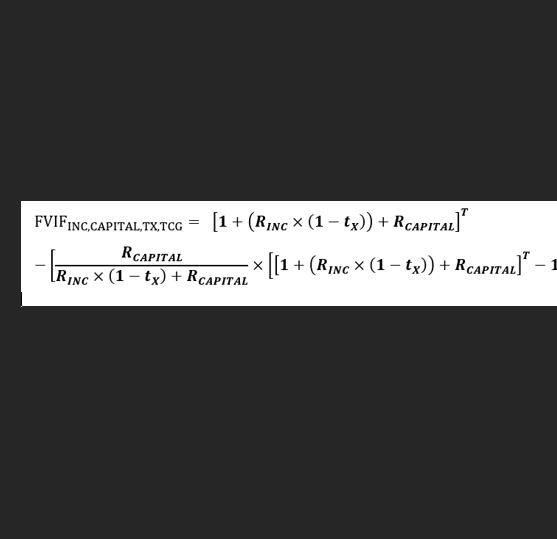

A guiding principle of Blue River Capital Management is to minimize our clients’ tax liabilities. One technique we use is converting traditional IRA assets to a Roth IRA during periods where the client’s marginal tax rate is low.

Converting traditional IRA assets to a Roth IRA is essentially a bet on your relative tax rate. When the conversion is made, the amount of the conversion is treated as taxable income, but your future tax liability is decreased because the value of the IRA will likely be lower than it would have been without converting. The general rule is this: if your current tax rate is lower than you expect your tax rate in retirement to be, you should convert. Roth conversions have additional benefits including:

- Locking in a known tax rate instead of having to navigate the uncertainty of what your future tax rate will be.

- Decreasing the size of your future IRA Required Minimum Distributions (RMDs) and your associated tax liability

- Roth IRAs have no RMDs, which could make them a better vehicle for transferring wealth to your heirs

For many investors, there is a window of opportunity where they can take advantage of a low marginal tax rate and convert traditional IRA assets to a Roth IRA. This window occurs in the period between the investor’s retirement and when they decide to take Social Security benefits. During this period, most people’s taxable incomes are quite low, which brings down their marginal tax rate. Note that the investor will need to fund their living expenses during this period from some other source, usually either a taxable brokerage account, savings account, or some other taxable source. While this conversion window after retirement is common for many people, it is not the only time to consider a conversion. Oftentimes, converting to a Roth IRA makes sense if someone’s income is lower than “normal”, such as if they are between jobs, taking time off work for any reason, or starting a new business.

Once the decision has been made to make a Roth conversion, it is important to keep in mind that investors can convert any amount of their traditional IRA in any given year. If a Roth conversion makes sense for an investor, we may advise making multiple conversions over several tax years in order to minimize the taxes paid up front. For example, if a client has a large IRA and retires at the age of 65, but can delay taking Social Security until age 70, it is highly likely it would make sense to convert traditional IRA assets to Roth IRA assets over the course of a few years. Typically, we would advise converting an amount that “fills up” their marginal tax bracket but does not unnecessarily subject them to higher tax rates. These Roth conversion ladders can save investors significantly on their tax bills, helping them reach their goals more comfortably.

If you have any questions about this blog, or other questions about your finances, please contact Blue River Capital Management at 503.334.0963 or at info@brcm.co.

This information is intended to be educational and is not tailored to the investment needs of any specific investor. Investing involves risk, including risk of loss. Blue River Capital Management does not offer tax or legal advice. Results are not guaranteed. Always consult with a qualified tax professional about your situation.