“Buy real estate for the tax advantages.”

“You can depreciate real estate and never pay tax on your income; with stocks you have to pay tax on the dividends.”

“I can just 1031 Exchange my real estate if I want to purchase a different property and never pay capital gains taxes. Or if I die, my heirs will get a step-up in basis.”

We have heard countless anecdotes from investors who staunchly believe in real estate that sound just like this. We must admit, the reasoning sounds great. Purchase a piece of real estate for investment purposes, depreciate it over a few decades to shield the rental income from taxes, then either hold onto it until you die or swap it tax-free for another property in a 1031 exchange. Sounds like the ideal tax-efficient investment, particularly when compared to stocks that force the investor to pay taxes on dividends and any realized capital gains. So what’s the problem?

Don’t get us wrong, we aren’t anti-real estate. In fact, we think it can be a great idea for many investors to hold both direct real estate investments along with a diversified portfolio of stocks (and maybe some bonds, too). We just believe the tax benefits of real estate are overrated, and the biggest culprit is property tax and its impact on returns.

Comparing the overall tax efficiency of different types of investments is not a straightforward task. In general, investments face three distinct types of taxes: income, capital gains, and wealth.

Income is easy enough: a stock pays a dividend, a bond pays interest, or a real estate investment pays out its net profits. All these forms of return are subject to income tax, and in the US, it is taxed at ordinary income rates (we will ignore tax-preferred income and dividends for today).

Capital gains are simple, too. You bought a stock for $10 and sold it for $20. You have to pay tax on the $10 gain, and, assuming you held the investment for more than one year, you get a lower tax rate.

Wealth taxes are less commonly thought about (though proposals to implement them have been making the rounds for years). Property taxes are a form of a wealth tax, as they are levied based on the value of the property, and investors in real estate must pay them every year. This yearly requirement can dramatically impact the after-tax returns for a piece of real estate.

How are investors able to compare the tax-efficiency of investments, particularly when different asset classes seem to be impacted by different tax regimes? It’s not easy, but it is possible. Enter our beloved CFA Tax Drag and Future Value Investment Factor formulas!!!

![]()

Yikes. They look intimidating, but the intuition behind them is simple. Using the two formulas above and some not-so-simple algebra, these formulas calculate the future value of a $1 investment over a period of time that is subject to income, capital gains, and/or wealth taxes. Now all we have to do is pull out our spreadsheet, put in some assumptions, and we can compare the tax efficiency of a hypothetical investment in real estate versus a portfolio of stocks.

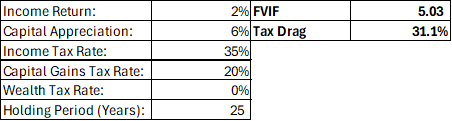

Let’s start with the portfolio of stocks and the following assumptions:

Plugging these figures in, our spreadsheet shoots out a FVIF of 5.03. This means, for every dollar invested, an investor would end up with $5.03 of after-tax value.

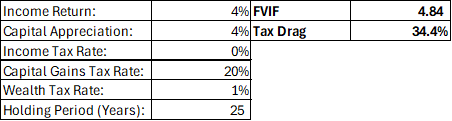

The real estate investment is a bit trickier; we will use the following assumptions:

In order to keep this a more “apples-to-apples” comparison, we kept the total return of both investments at 8% (total return equals income return plus capital appreciation) but assumed the real estate investment would have a higher proportion of that return come from income instead of capital appreciation. We also set the income tax rate for the real estate investment at 0% to account for the fact that real estate investors are allowed to shield income by depreciating the property. Finally, we assumed a property tax rate of 1% annually, which we found using our trusty AI agent (aka Google Search). With these assumptions, our spreadsheet yields a FVIF of 4.84.

Another way to think about these formulas is to calculate something called Tax Drag. The Tax Drag represents how much return is lost after all taxes are paid relative to a completely tax-free investment. The Tax Drag formula looks like this:

Using the figures from above, the stock portfolio has a Tax Drag of 31.1% compared to the Tax Drag of the real estate investment of 34.4%.

In this example, the real estate investment was actually worse from a tax perspective, even with the assumption that all income received over the course of the investment was tax-free. Of course, we could alter these assumptions and perhaps come up with a different conclusion, but we were somewhat surprised at how close these two figures came with what we view as very reasonable assumptions.

Some real estate tax superiority hold-outs may be screaming about now. “You assumed a liquidation at the end that resulted in capital gains, what about the 1031 Exchange? Or the step-up in basis to my heirs?”

Fair point, but stocks also receive a step-up in basis for heirs and there are some fairly slick ways to avoid capital gains taxes during investors’ lifetimes, as well (351 Exchanges, direct indexing, exchange funds, tax-loss harvesting).

Again, we want to emphasize we are not anti-real estate, but investors’ reasoning for purchasing it should likely not be for its tax benefits. In our opinion, the real opportunity in real estate is derived from its ability to be highly leveraged (usually 80%+ of asset value can be financed in a real estate transaction, compared to margin limits on a stock portfolio usually around 50% of asset value) at attractive rates (mortgage rates are significantly lower than margin rates) without the risk of a margin call if values drop temporarily. Of course, with high leverage comes high risk, so investors need to consider the consequences of such strategies, and the leverage advantage needs to be weighed against the higher transaction costs, illiquidity risks, legal liability, and time commitments inherent to real estate investing.

Blue River Capital Management, LLC is a registered investment adviser. This material is provided for informational purposes and is not a recommendation or advice. We do not provide tax or legal advice, and investors should consult their own qualified professionals regarding their individual circumstances. The analysis presented is hypothetical, for illustrative purposes only, and is not a guarantee of future results. There are material differences between the strategies discussed and assumptions used, which may not reflect actual performance, market conditions, applicable tax laws, or the circumstances of any individual investor. Tax laws are subject to change. Hypothetical performance has inherent limitations and does not reflect the impact of market conditions, liquidity constraints, or transaction costs. References to specific investment strategies are not recommendations and may not be suitable for all investors. All investments involve risk, including the possible loss of principal.