Do you remember in school when teachers encouraged raising your hand when you had a question because if you were wondering, somebody else probably has the same question?

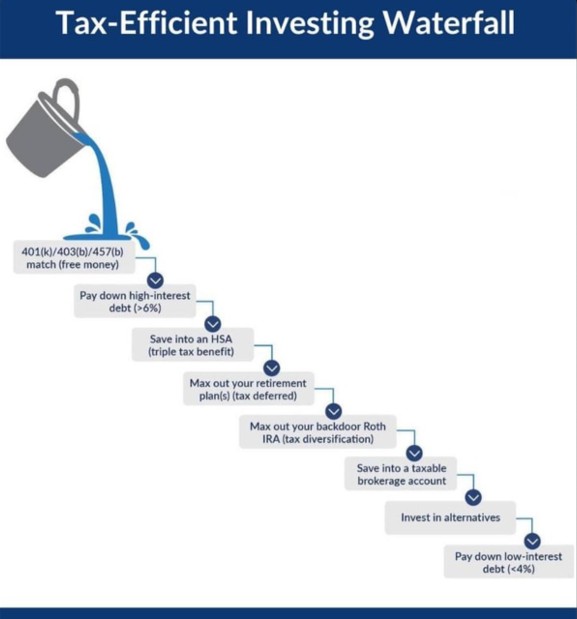

Well, we have recently fielded several questions about the backdoor Roth strategy, so we are guessing others are curious about them too. And, we would guess there’s a decent chance you have seen some graphic like this one on social media of an idealized tax-efficient savings strategy:

One of our first blog posts, The Excess Money Protocol, features a similar hierarchy. The logic is sound in both, and they are solid rules of thumb, but it’s so important to not follow them blindly because they gloss over a critical factor: you and your goals.

Before a couple examples, why and how do people do backdoor Roths?

Roth IRAs are attractive because they allow the money to grow tax-free and qualified distributions are not taxable (whether taken out by your or your heirs), so they’re great for tax-planning in retirement and estate planning. However, the IRS does not allow you to make Roth contributions if your modified adjusted gross income exceeds certain limits.

If your income does exceed the limit for making direct contributions, don’t despair! You can still get into a Roth IRA via the “backdoor”:

- Open – If you don’t already have one, set up a Traditional IRA.

- Contribute – For 2026, individual can contribute up to $7500 (plus an additional $1100 “catch-up” for those over 50). Preferably your contribution is non-deductible.

- Convert – Once the money is in your Traditional IRA, do a conversion to a Roth IRA.

Voila! You can rinse and repeat this process annually, or you can opt to do it every other year before Tax Day by doing a prior and current year contribution.

Deciding whether this strategy is right for you depends on your upcoming goals. Two recent client interactions highlight how the decision can vary.

On the surface, both clients are prime candidates: they live within their means, max out their employer-sponsored retirement plans, have no unproductive debts (high interest debts like credit cards or some auto loans), and are accumulating cash savings. However, one of them is potentially going to be making a real estate investment with her sister, in which case a little extra cash might be useful, so we decided that this might not be the year for a backdoor Roth conversion, but we have until Tax Day next year to decide.

We encounter other scenarios that occasionally take priority over an annual Roth conversion. Perhaps it’s to purchase a home, plan for education expenses, take a career break, start a business, or invest in something that’s not easily done through an IRA.

General advice, like the image above, is good in general but doesn’t necessarily translate to your situation, and we believe it’s important to understand when and how these rules of thumb should be bent or ignored to best help our clients accomplish their own financial objectives.

One complication with backdoor Roth conversions that is often overlooked is the IRS’s “pro rata rule.” If you have pre-tax money in any traditional, SEP, or SIMPLE IRA (401(k), 403(b) and 457(b) accounts are excluded), the IRS treats all those accounts as a single combined IRA when calculating the taxes on a Roth conversion. Unfortunately, you can’t tell the IRS that you are only converting your non-deductible contribution. Instead, the IRS will consider any conversion a proportional mix of pre-tax and after-tax dollars, which can create an unexpected tax bill or reduce the tax advantages of a backdoor Roth contribution.

If you have any questions about this blog, or other questions about your finances, please contact Blue River Capital Management at 503.334.0963 or at info@brcm.co.

This information is intended to be educational and is not tailored to the investment needs of any specific investor. Investing involves risk, including risk of loss. Blue River Capital Management does not offer tax or legal advice. Results are not guaranteed. Always consult with a qualified tax professional about your situation.